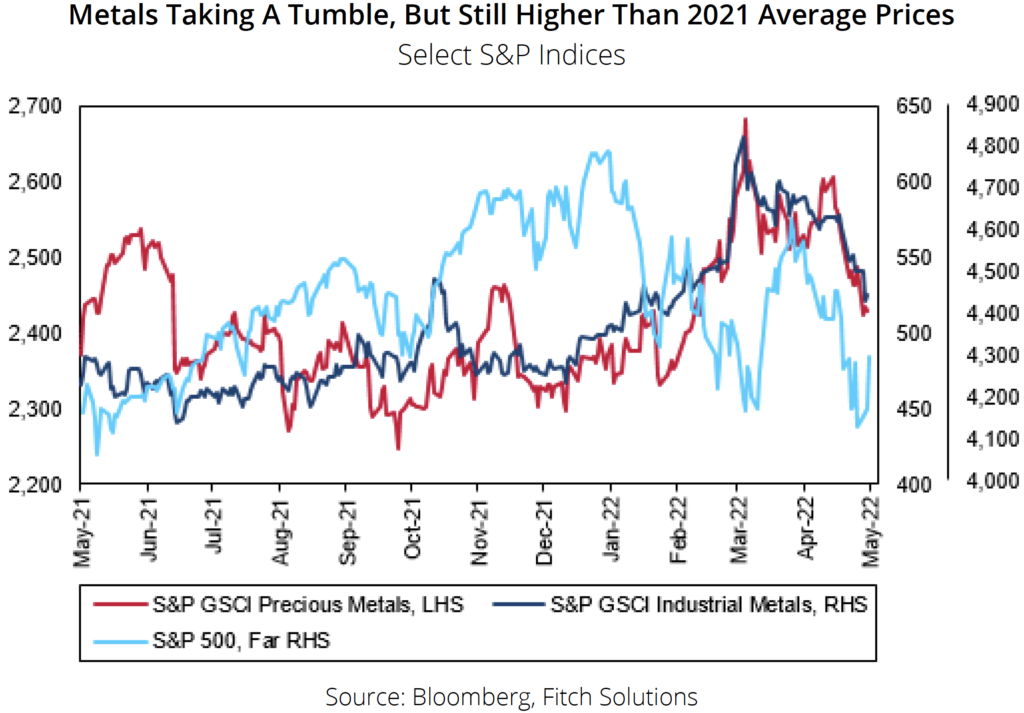

Enduring Covid-19-linked lockdowns in the world’s largest metal consumer, China, are negatively impacting demand from end-use industries and sentiment towards the complex, resulting in lower metals prices, a new report by Fitch Solution Country Risk & Industry Research notes.

Nevertheless, market analysts at Fitch maintain their 2022 metal price forecasts as prices generally remain above levels seen before the Russia-Ukraine conflict.

Fitch analysts also expect Chinese demand to eventually pick up in the second half, which will bring more stability to metals prices. Additionally, Fitch sees lockdowns in China as also acting to restrict supply. China is the world’s largest producer of metals, which will eventually drive prices to a balance in the coming months.

Fitch’s macro team expects further contractionary readings in both Chinese manufacturing and non-manufacturing purchasing managers’ indexes in the remaining two months of the current quarter. “Further lockdowns, either district-wide or full, have been imposed in more than two dozen cities around the country, with the capital Beijing having undergone three rounds of mass testing since late April. We continue to see downside risks to our 4.5% growth forecast for 2022, depending on further developments around lockdowns,” said Fitch analysts.

The analysts expects continuing loose fiscal and monetary policy in China through 2022 to help stimulate economic activity and growth, which should underpin demand for metals, particularly from the construction sector.

Fitch expects the Russian invasion of Ukraine to keep gold in the range of US$1,900 to US$1,800 per oz. in 2022 and 2023. The firm notes the deepening war situation has sparked an uptick in demand for the safe-haven asset as investors adopt a risk-off sentiment. While gold prices are hovering near their all-time high of US$2,075 per oz. and will be mainly dictated by the war in the coming months, Fitch expects U.S. dollar strength and recovering bond yields to cap gold’s rally.

“While we expect significant price volatility going forward, especially as the conflict in Ukraine evolves, we expect gold prices to remain elevated in the coming years compared to pre-Covid levels,” said Fitch.

Inflation rises

Meanwhile, Moody’s Investors Service expects relatively persistently high metals prices should help cushion the credit effects of cost inflation and generally lower production amongst senior miners in its coverage universe.

In a May 3 sector commentary, Moody’s said weaker mining production and volume constraints would exacerbate tight markets and further elevate prices of many metals. Several large rated global diversified mining companies posted first-quarter production results showing weaker production and rising costs following a buoyant 2021.

The high metals prices going into 2022 have provided a cushion to many mining companies that will help soften current market disruptions. Higher prices are likely to persist throughout this year, limiting the adverse effects of cost inflation on miners’ credit quality.

According to Moody’s, Covid-19-related labour constraints and cost inflation are the main drivers behind lower production and cost increases. At the same time, higher Covid-19 infections among workers have created labour challenges in crucial mining countries such as Australia, Peru and South Africa.

Compounding matters are weather-related disruptions impacting diversified miners operating in Brazil, South Africa and Australia.

Russia’s invasion of Ukraine in February has triggered turmoil in commodity markets, with Moody’s raising its near-term price assumptions for several metals and mining commodities to reflect constrained commodity supply.

Majors in murky waters

Moody’s notes that while Anglo American’s (US-OTC: NGLOY; LSE: AAL; ) credit metrics are expected to remain strong, with high commodity prices supporting margins and cash flow, it flags the potential for the major’s profitability and cash flow to be impacted by revisions to its guidance and other factors this year.

Anglo reported a 10% year-on-year drop in first-quarter production and lowered its full-year platinum group metals, iron ore and metallurgical coal production guidance. It also raised its overall cost guidance by 9%.

Anglo also suspended part of its metallurgical coal production because of a fatal incident at Moranbah, in Australia, in late March, with reopening subject to regulatory approval.

Weather or water availability issues may also continue to affect certain other operations.

Similarly, Moody’s notes that Glencore (LSE: GLEN) lowered its copper and cobalt full-year volume guidance by 3% and cut its zinc forecast by 9%, driven mainly by first-quarter developments.

However, it increased its guidance for nickel and ferrochrome by 3%.

While the production constraints for Glencore were largely driven by Covid-19-related labour constraints, geotechnical challenges and slower ramp-ups, Moody’s says the strong performance of coal, together with outperforming marketing operations, will continue to support growing profits this year.

A train transporting coal from Glencore’s Prodeco Calenturitas mine in Colombia. Credit: Glencore.

Further, Moody’s notes BHP’s (ASX: BHP) total group production (excluding petroleum operations) decreased by 3% on a copper-equivalent basis for the nine months ended March 31, mainly because of lower copper volumes.

Pandemic-induced labour issues contributed to BHP’s March quarterly copper production, registering 6% below the comparable period last year and reflecting lower grades and disruptions from public road blockades near Escondida, in Chile, its largest copper mine.

Also compounding matters in Moody’s’ view is BHP lowering its copper production guidance for the fiscal year ending June 30.

However, despite similar labour challenges and ongoing cost pressures across its iron-ore and metallurgical coal operations, BHP critically maintained its production and unit cost guidance.

This will support continued strong cash flow generation, as iron-ore is BHP’s most significant earnings contributor and metallurgical coal benefits from record prices.

Further, Vale (NYSE: VALE) maintained its iron-ore production guidance for 2022 at between 320 million and 335 million tonnes, despite the challenges it dealt with in the first quarter when heavy rainfall temporarily stopped production at the Southern and South-eastern systems and led to stoppages of railway transportation in the Northern system.

Some delays in obtaining licences and maintenance works also contributed to the overall 6% decline in iron ore production volumes in the first quarter compared with the same period in 2021.

Yet, according to Moody’s, improved production capacity in Minas Gerais and the Northern system will support the production guidance this year.

Although Vale’s cash costs for iron-ore increased by US$2.20 per tonne to US$18.70 in the first quarter, the miner estimates its cash costs for iron ore (excluding third-party purchases) will remain between US$18.50 and $19 per tonne this year.

Despite these challenges, Vale’s cash flow will benefit from elevated iron-ore prices and sales with a higher share of premium products.

Also in its coverage universe, Rio Tinto’s (NYSE: RIO; LSE: RIO; ASX: RIO) Pilbara iron-ore segment – accounting for 59% of revenue and 72% of the earnings before interest, taxes, depreciation and amortization in 2021 – reported a 6% year-on-year decline in production and an 8% decline in shipments in the first quarter, mainly owing to labour shortages and supply chain issues.

Moody’s points out that Rio Tinto reiterated its 2022 iron-ore unit cost guidance of between US$19.50 per tonne and US$21 per tonne and shipments guidance of between 320 and 335 million tonnes.

The figures remain subject to many operational risks, including the commissioning and the ramp-up of the Gudai-Darri greenfield mine in Western Australia and brownfield mine replacement projects, uncertainty around the impact of cultural heritage management on mine plans and Covid-19-related constraints.

Be the first to comment on "Plunging metals prices expected to rebound in H2 – report"