Are we living in the 1970s? I can’t tell you, I wasn’t there, but it’s an interesting analogy.

Then, as today, we have the fear of inflation, the eroding value of cash and now spiking oil prices.

Of course, nothing can repeat exactly. The event that’s said to have launched hyperinflation in the 1970s, the Yom Kippur War, only lasted 20 days. As we go to press, we’re now past the 30th day in this Iranian conflict with the U.S. and Israel.

So, maybe we’re not living in the 70s at all, but something far worse? But it’s not so much the war that’s important here; it’s the flow of oil.

For now, the Strait of Hormuz remains shut except for a few renegade exceptions, like Japan. The Japanese government was reportedly in talks with Iran to ensure the safe passage of its oil vessels moving through the strait.

As a long-term ally of the U.S., it’s a meaningful development that highlights that when push comes to shove, energy matters more than friends. Japan funnels about 90% of its oil shipments through this strait. No doubt, it’s keen to make a deal.

As I said, oil flow matters more than the war itself. And gradually, ships are leaking through the strait. There were also reports that Iran was charging vessels a $2-million “toll fee” to pass through. That’s assurance for tankers that they won’t be sunk if they pay up.

Could those who pay the toll secure lower insurance premiums? It’s another unknown that could free up the bottleneck. But it could also provide Iran with a critical source of additional war revenue. Capitalism is alive and well in the Iranian regime.

Pre-war, up to 140 ships passed through the strait daily, including roughly 60 oil/gas tankers. It seems Iran now has an opportunity to finally monetize its geographical advantage.

Let’s assume the daily count lifts to just a fraction of these pre-war numbers in the coming weeks; it could help sustain Iran’s war effort against the U.S. and Israel.

And that’s potentially putting into motion a war that goes into deadlock rather than resolution.

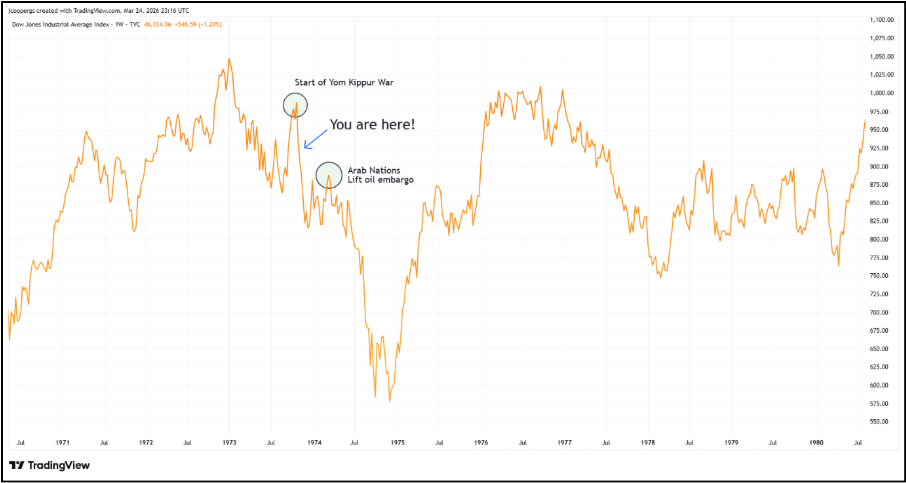

Lesson of 1973

While the Yom Kippur War lasted just 20 days, oil flows to the West remained closed for much longer than that. Arab producers continued a strict oil embargo against the West for around five months as retaliation for their support of Israel in the Middle East.

And once oil began to flow (post-embargo), oil prices remained stubbornly high. But the consequences went far beyond that.

Six months after the Yom Kippur War began, the US Dow Jones Industrial Average fell 17% from its 1973 peak.

But the real stock market crash didn’t take place until July 1974, about eight months after the start of the conflict. And that’s the timeline that should be on investors’ radar.

From the 1973 pre-war peak to the 1974 stock market bottom, the DJI fell 45%. It’s not unreasonable to assume that today’s richly valued tech-heavy Nasdaq would have fared much worse back then.

Source: Trading View

It’s conceivable, too, that oil flows could remain constricted for a similar duration, like in the 70s, where embargoes remained in place for five months. And when those embargoes were finally lifted, rather than easing pressure on financial markets, markets revolted. The damage was already baked in.

By July 1974, U.S. interest rates were breaching double figures. And markets entered a cyclical bear market. But despite broad weakness across financial markets, the outlier remained commodities, particularly energy. Oil futures traded for a measly $3.50 per barrel prior to the Yom Kippur War in 1973. Postwar, they climbed above $10 per barrel. And by the end of the 1970’s, oil was trading above $30 per barrel. About 750% higher from the start of the decade!

Could that happen again? Let’s hope not. Before events in Iran, oil traded at about $72 per barrel. The shock came as oil tipped past $100 per barrel, delivering a mere 40% increase. That was well below the 1970’s oil price shock.

So, clearly, there are differences, and you can’t take the 1970s as a one-for-one blueprint on what will happen next.

And while it does have its limitations, for investors, using historical analogies like this could prove far more useful than the hyperbolic news cycle.

The 1970s is a helpful yardstick; follow it wisely.

James Cooper is a geologist based in Australia who runs the commodities investment service Diggers and Drillers. You can also follow him on X @JCooperGeo.

Be the first to comment on "Opinion: The world of cheap oil is gone"