With the increasing adoption of electric vehicles (EVs) and energy storage technologies, there is little doubt demand will grow for battery raw materials that must be sourced from the mining industry.

We expect automotive companies and battery manufacturers to invest US$300 billion in the sector in the next 10 years, and they will require new battery mineral deposits to be developed.

However, given the current climate of underinvestment in the mining sector, will future supply be able to meet these projections of rapidly increasing demand? The answer is not clear.

Over the next 10 years, we expect demand related to battery raw materials to increase four times for lithium, five times for cobalt, and up to seven times for graphite.

Beyond that, vanadium will be required in increasing volumes for use in stationary batteries for energy storage in renewable energy installations, while rare earths already have a place in high-performance magnets widely used in electric motors and wind turbines.

Against this background of anticipated growth in demand, technology is continuously improving in the battery sector, as manufacturers lower costs and improve performance in an effort to encourage higher adoption rates.

For example, EV battery manufacturers face pressure to increase energy density, decrease recharging time, reduce weight, and improve cold weather performance and safety.

Battery raw materials currently make up half the cost of battery cell manufacturing costs.

To realize these performance enhancements, manufacturers are demanding increased quality of raw materials. To be competitive on the cost curve, suppliers of lithium, cobalt and graphite feedstock will be pushed to achieve higher processing efficiencies.

Processing innovation

There will be pressure on the supply of specialty raw materials, and new deposit types are already being assessed for economic viability.

Innovation in mineral extraction and process development is needed to meet the challenges posed by end-use markets — especially in green technology, renewable energy and battery applications.

Already, physical and chemical specifications on mineral products and processed materials are only getting more stringent. Many products must reach 99.99% purity (“four nines”), but even more pronounced are the impurities themselves, at the parts per million level, as they risk affecting the performance of the final product.

Processing innovations in the lithium sector are focused on hard rock minerals, such as spodumene, petalite, lepidolite and mica, and on lithium-bearing clays, to produce lithium carbonate and lithium hydroxide for batteries.

Physical beneficiation results in a mineral concentrate that is processed by calcination and acid leaching.

Spodumene remains in focus, since the lithium content is higher than for other sources. But other minerals could offer advantages.

For example, lithium-bearing clays are relatively soft and easy to mine, and may be processed acid-free. In contrast, various hydrometallurgical processing routes are under development for spodumene and petalite offering the advantage to produce lithium hydroxide directly, without going through the carbonate stage.

This lowers energy and reagent consumption, and achieve higher purity and improved cost competitiveness against lithium brine sources.

Cobalt is generally produced as a by-product of copper and nickel, and is driven by the economics of those industries.

To meet the projected needs of the battery sector, cobalt is not expected to be sourced from by-product production alone. New production from primary cobalt projects will be needed to fill the supply gap.

There are also inherent risks in the dependency on the major producer of by-product cobalt, the Democratic Republic of the Congo, and on cobalt-processing facilities that are Chinese-controlled.

Existing producers of cobalt are boosting production of cobalt chemicals for battery applications, particularly in the form of cobalt sulphate.

As potential new entrants to the market, primary cobalt developers look at projects where cobalt is recovered from more complex mineralization, but they can take advantage of innovative process flow sheets to directly produce battery-grade cobalt sulphate.

Similar to lithium minerals, natural graphite is beneficiated by comminution, careful liberation and multiple flotation stages to recover a high-grade (+98.5%) concentrate, but must be further processed so that material is suitable for batteries.

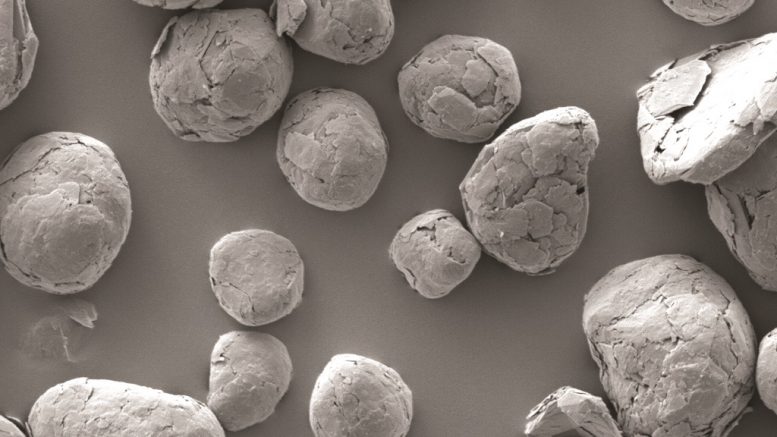

A spheroidization process is used whereby graphite flakes are folded and wrapped into a sphere known as a “potato.” Spheroidization preserves the original flaky structure — i.e., the flake size and aspect ratio — which allows rapid passage of lithium ions, while the potato shape allows the graphite to be packed most efficiently into the battery anode.

Innovation is applied to the spheroidization process to improve the typical yield rates from 30–40% to 60% or more, which improves economics by lowering the amount of less valuable fines.

Final impurities in the battery grade graphite must be less than 0.05%, or 500 parts per million. Innovative methods look to achieve this purity by methods free of hydrofluoric acid, such as thermal technologies, or the introduction of less harmful reagents for treatment.

Vanadium

There are relatively few sources of primary vanadium, and the steel industry accounts for nearly 90% of total demand, with chemical catalysts accounting for almost all of the balance.

Vanadium redox batteries for grid energy storage are finding a wider range of applications, but there are concerns over the availability of supply, despite the fact that vanadium is more abundant in nature than lithium.

Changes in China’s high-strength rebar standard to support prior modifications in building codes include high-vanadium-content concrete rebar, which has prompted additional assessment of alternative vanadium sources.

A potential source includes waste steel-making slags, which can be reprocessed to recover a suite of products, including ferrovanadium, high-purity steel and clean slag. An innovative approach to processing vanadium-bearing waste slags involves combining pyrometallurgical and hydrometallurgical steps, and, particularly, the use of high-temperature roasting of the slag.

The economies of scale needed to be achieved for the electrification of the automotive industry must also be matched by raw material producers, even as the environmental impact of mining operations and mineral extraction plants are kept to a minimum.

Anticipated increases in demand — with limited supply sources —will drive the mining industry to primary sources, often with increasingly complex mineralogy.

Innovation drives end-use markets, and, in turn, this results in innovative flow sheets and adoption of new process technologies.

— David Anonychuk is managing director of M.Plan International, while Jane Spooner and Reiner Haus are both co-chairs of M.Plan.

M.Plan was founded in 2015 as a joint venture between Dorfner ANZAPLAN of Hirschau, Germany, and Micon International of Toronto to provide integrated services to the specialty minerals and metals sector. Due diligence reviews, preliminary economic assessments, pre-feasibility and feasibility studies are generated to meet the requirements of international securities regulations, such as National Instrument 43-101, and JORC. For more information, visit www.mplaninternational.com.

I found this article to be informative and challenging. I think we all like the concept of electric vehicles however we wonder if it can be as viable long term as gas and diesel powered vehicles.

A well worded comment Doug. I find that a lot of scientific minded people question the viability of electric vehicles and “green” power in general once the government incentives/rebates/etc (taxpayer funding actually) disappears. Germany is experiencing this and companies such as Tesla are feeling the pinch in Ontario now that the incentives are gone. Most non-government funded scientists know that the CO2 fear factor and “carbon” taxation is one of the biggest scams that this world has seen to date. Now just waiting for the blow back on this one from the left and IPCC cheerleaders.