AGADIR, MOROCCO — Mosaic (NYSE: MOS) may be the largest producer of finished phosphate products in the world, with four phosphate-rock mines, three processing plants in Florida and a second plant in Louisiana, but permitting new mines or extensions to existing ones in the southern U.S. state can be a nightmare, with wait times that can last a decade.

At the same time, the Plymouth, Minn.-based producer is trying to preserve its status as the largest phosphate-fertilizer exporter to India against inroads by Chinese and Saudi Arabian producers, and is importing phosphate rock from Peru and Morocco — a country with the largest phosphate-rock reserves on the planet. Phosphate rock is the primary source for phosphorus, one of three elements along with nitrogen and potassium that is critical to plant growth and used in phosphate fertilizer.

In July Mosaic signed an agreement with Saudi Arabian Mining (Ma’aden) and Saudi Basic Industries (SABIC) to bring into production a US$7-billion greenfield phosphate project called Wa’ad Al Shamal along Saudi Arabia’s northeastern border with Jordan. Wa’ad Al Shamal is expected to start production in late 2016 with a capacity of 3.5 million tonnes of finished phosphate per year.

Mosaic will invest US$1 billion over four years starting in 2013 and contribute expertise to the design, construction and operation of the facilities. In exchange it gets a 25% ownership stake in the project and the right to market a similar quantity of the phosphate fertilizer and animal feed the venture produces.

“Mosaic knows that they are likely to eventually lose shares in India to Chinese and new Saudi Arabian production, and this was a factor in Mosaic joining with Ma’aden’s second plant to invest its way back into more Indian market share,” Joel Jackson of BMO Capital Markets says in an interview.

“It’s a clever move,” says Alberto Persona, a specialist on phosphates and potash at CRU, a privately held market analysis and consultancy firm in London, emphasizing the role permitting delays in Florida have had on Mosaic. “The process to obtain new permits in Florida is lengthy and painful. It took nine years of permitting for Mosaic to clear the South Fort Meade mine in Hardee County. You need approvals from roughly twelve different bodies to get permits — that’s why it takes so long.”

“They’re trying to get new mines permitted, but there are a lot of legal issues in Florida trying to get that done,” Stephen Jasinski of the U.S. Geological Survey confirms. “That’s one of the reasons why Mosaic is entering into these joint ventures.”

The deal with the Saudis is about far more than circumventing permit holdups in Florida, where Mosaic estimates current and future reserves will allow it to mine phosphate rock for the next 30 to 35 years. It’s about tapping into growing phosphate markets more quickly and cost efficiently in countries like India, where Mosaic has a network of terminals, inland distribution points and infrastructure. And shipping phosphate fertilizer from Saudi Arabia will be a whole lot cheaper than sending it all the way from Florida, CRU’s Persona says. Moreover, Ma’aden is the lowest-cost producer of diammonium phosphate (DAP), the product preferred by Indian farmers.

“With Mosaic’s investments on the distribution side in India and with a strong, aggressive partner like Ma’aden, which wants to be one of the world’s major phosphate producers — like BHP Billiton (NYSE: BHP) hopes to be someday in potash — the deal will be beneficial for Mosaic. It’s hard to know for sure, but it could lower Mosaic’s cost of sales by as much as US$50 per tonne.”

Monica Baker, research manager of fertilizer consultancy at Integer Research, says that the export-oriented project in Saudi Arabia will be a major player in the future. “In the last decade, most of the phosphate expansion activity took place in China,” says the London-based analyst. “But we can see now how other regions of the world — including Saudi Arabia and Jordan in the Middle East, Morocco and Tunisia in North Africa, as well as Brazil — are taking centre stage, while Chinese expansions are set to slow in the next few years.”

Describing it as a significant development for the industry, Baker points out that the deal brings together access to competitively priced raw materials (i.e., phosphate rock, ammonia and sulphur) and proximity to the customer base, which makes a big difference to the prices companies processing phosphate fertilizer can get for their product.

Robb Litt, a spokesman for Mosaic, says the decision to pursue the joint venture with Ma’aden and SABIC is part of the company’s growth strategy and “has nothing to do with permitting in Florida,” which he concedes takes on average between five and ten years.

“Our Florida mine sites are capable of meeting the needs of our fertilizer plants, but the ability to be flexible with our rock sourcing in the future may be an opportunity,” he says, adding that the company’s Hookers Prairie mine will be mined out in 2014; its Four Corners mine in 2020; and its South Fort Meade mine in 2021. Mosaic doesn’t expect to mine phosphate rock at its Ona project until 2020, and at its DeSoto project until 2021.

“The Ma’aden SABIC joint venture will align us with the lowest-cost production of phosphate crop nutrients, and will position Mosaic in close proximity to emerging markets in India and Southeast Asia,” Litt explained in an email after declining an interview. “The joint venture will enhance our competitive position in the global marketplace by diversifying our sources of phosphate rock while improving our access to key geographies . . . when complete, the new operation will be one of the lowest-cost phosphate producers in the world.”

The Saudi partnership also builds on Mosaic’s other efforts to nail down phosphate-rock supplies — the feedstock for phosphate fertilizer and phosphoric acid. There are no substitutes for phosphorus in agriculture and 85% of the phosphate produced is used to make fertilizers, and the other 15% as an input for animal feed, detergents, metal processing, preservatives, pharmaceuticals and food supplements.

Under a joint-venture agreement with Vale (NYSE: VALE) and Mitsui of Japan, Mosaic has rights to 35% of the phosphate-rock concentrate produced from the Miski Mayo mine in the Bayovar region of Peru. Next year Miski Mayo will produce 3.8 million tonnes of rock. Mosaic’s share — 1.3 million tonnes — will be consumed at its Louisiana processing plant in the U.S. and by Mosaic’s other consumers of the rock at its operations in Brazil and Argentina.

Mosaic, like other phosphate-fertilizer producers, has turned to Morocco — a desert kingdom in North Africa with an estimated 89 billion cubic metres of phosphate rock, the largest reserves in the world. Mosaic imports phosphate rock from state-owned producer Office Chérifien des Phosphates (OCP). Potash Corp. of Saskatchewan (TSX: POT; NYSE: POT) also has a deal in place with OCP — importing 6% of the phosphate rock it processes company-wide from the Moroccan company — while Agrium (TSX: AGU; NYSE: AGU) will import rock from OCP at the beginning of October, when its mine in Kapuskasing, Ont., expires.

“North America’s

rock capacity is set to decline sharply in the early 2020s, and some phosphate-fertilizer producers have already tied up contracts with OCP or are importing from other origins, or are looking for alternative suppliers,” Baker of Integer says. “Morocco is the largest rock seller in the world and is likely to keep its position at this stage.”

In a January 2012 report on phosphate rock from the U.S. Geological Survey, world phosphate-rock production is projected to increase by nearly 20%, from 215 million tons (195 million tonnes) in 2011 to 256 million tons (232 million tonnes) in 2015, with most of the increase occurring in Africa and the largest increase expected from Morocco.

In its literature, OCP says Morocco’s known reserves are “sufficient to meet several centuries of demand,” and claims it supplies 37% of the world’s phosphate rock, half of its phosphoric acid and 15% of its fertilizers (it counts itself among the five largest phosphate-fertilizer companies in the world) from four mining centres and nine chemical-manufacturing facilities.

Last year the company generated revenues of 59.3 billion dirham (US$7.12 billion). Half of its phosphate rock is exported as raw material to 40 countries around the world. The other half is sent to its chemical production facilities and turned into basic phosphoric acid, purified phosphoric acid and phosphate fertilizers.

“Morocco has much more high-quality rock remaining compared with the U.S., and companies like Mosaic and others are trying to prolong their resources,” Jasinski of the U.S. Geological Survey says.

Richard Downey, vice-president of investor and corporate relations at Agrium, says its phosphate facility in Redwater, Alta., used to import phosphate rock from Togo in West Africa until the company opened its Kapuskasing mine in northern Ontario in 1998. Agrium also has a phosphate-rock mine in Idaho near its phosphate production facilities and has a phosphate production plant and a phosphate-rock mine in Idaho that it acquired in late 1997. It has access to more phosphate-rock reserves on lands leased mostly from federal and state governments in the U.S. under long-term arrangements.

But Agrium started looking for alternative sources of supply several years ago ahead of the scheduled closure of its mine in Kapuskasing. In September 2011, Agrium executed a long-term rock agreement to 2020 with OCP, and will start receiving Moroccan rock in October. Under its deal with OCP, Agrium will pay more for the rock when international prices for phosphate fertilizer are high and less when prices fall, which reduces risk.

“We looked all over the world at a variety of sources, and obviously Morocco has got some of the largest reserves and the best grade out there,” Downey says. “There are some reserves in the Western U.S. that we continue to evaluate, and we’re doing some exploration in Utah. But permitting is an issue, and that’s why we did the deal with OCP.”

OCP’s monopoly on phosphate rock means that it can control the prices it charges and squeeze the margins of integrated fertilizer producers and distributors. In a corporate presentation by Stonegate Agricom (TSX: ST; US-OTC: SNRCF) citing 2012 estimates from the U.S. Geological Survey, seven countries in the Middle East and North Africa account for 83% of the world’s phosphate-rock reserves, 24% of phosphate-rock concentrate production and 77% of the world merchant market. Of the merchant market, Morocco’s share is 35%.

OCP claims the quality of its phosphate rock — measured by the percentage of phosphorous pentoxide (P2O5) it contains — is among the best in the world. Grades for phosphate deposits can run anywhere from 4% P2O5 to 35% P2O5, but a marketable concentrate typically needs to be at least 28% P2O5.

“Morocco probably has the highest grade of P2O5 of the world’s sedimentary deposits, which are the bulk of world production,” Jasinski of the U.S. Geological Survey confirms. But he says the highest grade rock comes from igneous deposits found in Russia, South Africa and Finland.

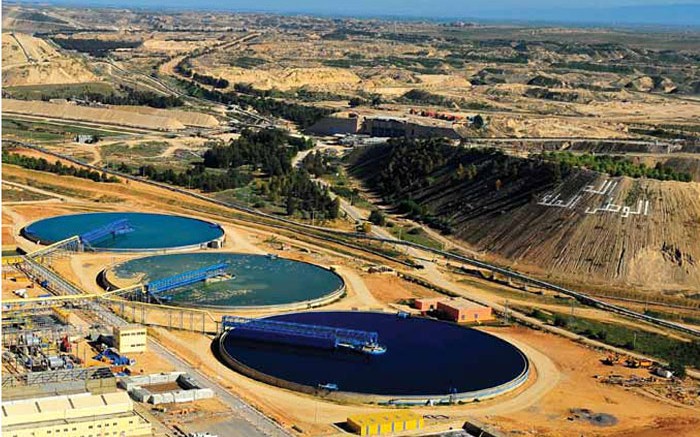

Morocco’s sedimentary deposits were formed 70 million years ago in layers of maritime bedrock. On a site visit earlier this year to Khouribga — one of OCP’s mining centres and its largest phosphate production zone, with reserves of 25 billion cubic metres — about a 120 km drive southeast of Casablanca, visitors watched a dragline operator scrape rock from a beach-white sedimentary deposit in an open pit under blinding sun and temperatures approaching 40 degrees.

OCP plans to double its phosphate-rock production to 50 million tonnes a year by 2020 and boost its processing capacity for DAP (the most commonly used fertilizer) and of monoammonium phosphate (MAP), (a fertilizer consisting of phosphorus and nitrogen). Its plant at Jorf Lasfar has a capacity of 3 million tonnes a year of DAP and MAP fertilizer, and says it will add another 4 million tonnes a year of capacity by July 2015. Management claims this figure will rise to 13 million tonnes by 2020.

OCP is the biggest rock producer in the world and the third-biggest fertilizer producer, and it accounts for the biggest share of investments globally, both upstream in terms of mining capacity and downstream in terms of phosphoric acid and fertilizer, Persona says.

“It’s a huge company and wants to get stronger and stronger,” Persona says. “The ease of obtaining permitting and access to relatively cheap capital is indeed an advantage when planning a wave of world-scale expansions; other competitors can hardly enjoy a similar environment. Moreover, the shallow geological structure of Moroccan deposits makes it relatively faster and inexpensive to expand mining capacity.”

The company has earmarked US$12.2 billion dollars to expand its phosphate-rock mines, chemical processing facilities and infrastructure, and is building a 300 km underground slurry pipeline connecting the Khouribga phosphate-rock mine to the company’s chemical processing hub at the port of Jorf-Lasfar.

The slurry pipeline is part of OCP’s strategy to become the industry’s lowest-cost producer and could be complete before year-end. The slurry will travel at 5,000 cubic metres per hour and take seven hours to reach Jorf-Lasfar. OCP says moving the rock via pipeline will reduce the company’s mine-to-port costs, cut energy and water use, carbon dioxide emissions and potential environmental degradation.

OCP site director Abdel Kader Alouani, who led visitors around the mine site in May, declined to address questions from The Northern Miner on exactly how much money the slurry pipeline would save the company on transportation costs. But on its website OCP says the pipeline will cut transportation costs to less than US$1 per tonne from US$7 to US$8 per tonne.

OCP has generated some controversy in recent years, however, not only because some of its phosphate production comes from the Western Sahara — a disputed area bordered by Morocco in the north, Algeria to the northeast and Mauritania to the east and south that Morocco claims is its own — but because the company discharges untreated waste from its phosphate production directly into the sea. “They pump it into the ocean where it gets dispersed,” Jasinski says, “but they say they plan to stack it in the future.”

The waste product — phosphogypsum — is commonly referred to as gypsum or calcium sulphate. It is a

by-product fertilizer production that is created when sulphuric acid reacts with phosphate rock to produce the phosphoric acid needed for making fertilizer.

Traditionally, phosphogypsum is pumped into stacks adjacent to manufacturing facilities and stored there permanently. In China, phosphogypsum is used in the construction industry (i.e., building materials, cement, wallboard, bricks and road work), but because the material often contains traces of radioactivity its use is restricted in most countries.

Mosaic says it invests research and development money internally and works with the Florida Industrial and Phosphate Research Institute seeking ways to improve gypsum stack management. In the meantime, the company says “properly designed gypsum stacks are the most environmentally responsible way to manage and store gypsum in compliance with existing regulations.”

At an international conference on phosphates sponsored by OCP after the site visit to its operations, executives from the state-owned company and Dupont announced they had set-up a fifty-fifty joint venture that would provide consulting and training “to improve the safety, operational and environmental performance of companies in Morocco and other African countries.”

Simon Herriott, Dupont’s managing director of consulting solutions, confirmed that the joint venture would operate before 2014 and would help companies throughout Morocco and northwestern Africa — including OCP — improve performance, safety, productivity and sustainability, but declined to comment on issues or challenges, including whether or not it would address OCP’s practice of dumping phosphogypsum into the ocean.

Speakers at the Symphos conference in Agadir also noted that phosphate is an energy mineral because it contains uranium, thorium and rare earth elements, and research is being conducted on extracting these elements from phosphoric acid and phosphate rock.

As far as phosphate-rock prices are concerned, up until April 2007 they were fairly steady, running at US$45 per tonne freight-on-board Morocco, Persona of CRU says. But spikes in fertilizer commodity markets pushed the price of the rock up to US$430 per tonne in September 2008. By July 2009 prices had fallen back to the US$90-per-tonne level. They crept back up again in 2010, and over the last two years have stayed within US$160 to US$200 a tonne, even though they have showed a decline to the current level of US$145 a tonne since 2012.

Mosaic expects annual growth in the consumption of phosphate crop nutrients will remain at 2% a year, which it argues should ensure stable to increasing prices.

Meanwhile, with traditionally high margins on phosphate-rock sales, a number of juniors have been attracted to the industry in recent years — particularly in countries like Brazil — and they have unveiled new projects.

“Junior miners were attracted to the phosphate-rock space by the strong profitability in the industry — in 2010 and 2011, especially — and by a strong, demand-driven market,” says Baker of Integer Research in London. “The high value of rock has been attractive to these companies. In 2012 profitability dipped for a number of reasons, such as lower demand from the key Indian market [after subsidies were withdrawn], higher input costs and lower revenue due to lower phosphate prices.”

Baker argues that projects will go ahead based on favourable cost structures, rock quality and proximity to customers. “Most of the junior-mining projects are positioned at the higher end of the cost curve, and will need to achieve a decent rock price to make the project attractive to investors,” she says.

But Jackson of BMO Capital Markets believes that most won’t go into production. “Only a couple will get done,” he says. “Maybe when the next investment up-cycle comes around.”

Paul Burnside, manager of fertilizer analysis products at CRU, notes that OCP has leverage because “the thing with [phosphate] rock is that the reserves in Morocco are just vast — absolutely vast — so in principle it could bring on as much capacity as it wanted, and I think that may be one reason that there hasn’t been as much activity in phosphate development as in potash, in terms of the juniors. OCP has millions and millions of tonnes of capacity. A lot of the junior projects are looking at much smaller tonnes.”

But while OCP often acts as the swing producer, Integer Research’s Baker argues that OCP has proved in recent years that it’s responsive to international market conditions, and its production and exports are likely to be sensitive to market developments. “Much of the new investment can be phased in at intervals,” she says, “and is likely to be influenced by market developments. The company has also taken capacity out of the market at times, in response to weaker market conditions.”

Over the next five years expect lots of good news on phosphate from Quebec. Investissement Québec and Yara building Mine Arnaud at Sept-Îles and Arianne and Jourdan developing projects in the same rock package to the west close to Baie-Comeau and Saguenay. With Agrium shutting down production in Ontario at Kapuskasing – being the only Canadian phosphate mine, Mine Arnaud when it comes on stream will be the only Canadian Mine, and as Arianne gets closer to a production decision, and Jourdan gets closer to completing a maiden 43-101 resouce, Quebec should become the largest resource of phosphate in the world outisde of Morocco.