VANCOUVER — An offtake agreement with a US$50-million prepayment has given Mawson West (TSX: MWE; US-OTC: MWSWF) the funds it needs to finish building its Kapulo copper–silver mine in the Democratic Republic of the Congo.

Kapulo will be Mawson’s second mine and processing plant in the DRC. The first, Dikulushi, was a historic operation that Mawson refurbished and restarted in mid-2010. The open-pittable resource at Dikulushi has been depleted, so Mawson moved underground at the site. However, defined underground resources at Dikulushi can only sustain the operation for another six months.

The idea was to finish Kapulo before then to secure more copper production, but in recent months Mawson had slowed its work at Kapulo to conserve capital, putting that timeline in jeopardy.

Now an offtake deal with privately held commodities trader Trafigura Beheer has Mawson’s plans back on track. Trafigura will buy 100% of the copper concentrate produced at Dikulushi and Kapulo for 48 months, starting once Kapulo reaches commercial production. In exchange, Trafigura is providing Mawson with a US$50-million prepayment, available immediately.

“This is a good deal and we’re pretty excited about where we are going from here,” said Mawson CEO Bruce McFadzean in a conference call.

The US$50 million has to be repaid in eight installments starting in March 2015. Mawson says the loan has competitive fees and rates and does not carry any hedging conditions. On the offtake side, the partners did not disclose details, but describe the terms as standard-industry payable with international benchmark treatment and refining charges, and competitive transport charges.

“This deal took a bit longer than expected but we targeted several parties, and I can proudly say that Trafigura provided a lot of clarity and this is a well-supported arrangement,” said Greg Entwistle, Mawson’s chief operating officer. “This is a well-structured arrangement and [the terms] give me comfort that this is a fairly flexible arrangement for Mawson, and one that we can move forward with.”

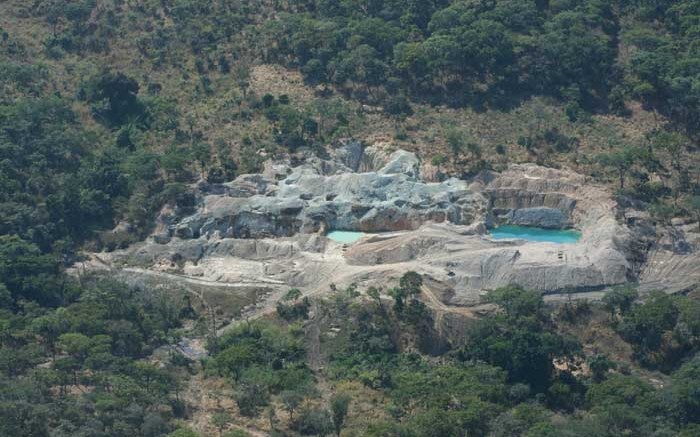

The focus will now shift to the half-built Kapulo mine. Kapulo’s feasibility study pegged capital costs at US$124 million. Mawson has already spent US$77 million at the site, where all civil works are completed and the bins, feeders, crushers, screen decks, ball mills, coarse-ore tunnel and flotation circuit building are installed.

“The prepayment means the remaining capital expenditure required for Kapulo is now secured,” McFadzean said, adding that all the long lead-time items have been ordered and commissioning is expected during the fourth quarter.”

When Mawson completed the Kapulo feasibility study only one of the project’s three outcropping deposits was defined to reserve status. That deposit, known as Shaba, was enough to produce 20,000 tonnes copper in concentrate annually over six years.

In January Mawson updated the Kapulo resource estimate, based on another 16,530 metres of drilling. The effort grew the project’s overall resource count, and added confidence to the resources at Safari North and Safari South.

Overall, the project’s three deposits offer 6.23 million measured and indicated tonnes grading 3.02% copper and 2.87 million inferred tonnes averaging 2% copper. Mawson is working to update the feasibility study and incorporate the new Safari North and South resources.

Shaba is a tabular deposit that strikes 460 metres and averages 30 metres wide. It dips moderately west and has been tracked 350 metres deep, still open down-plunge. The deposit includes a discrete hangingwall zone wherein copper grades regularly best 6%.

At Safari North the main mineralization body strikes for 430 metres and ranges 10 to 45 metres wide. It has a higher-grade core zone and has been defined to 180 metres depth, and remains open. Safari South has a similar shape but has only been tested to 65 metres depth. In addition, Safari South averages 1.6% copper compared to a 2.51% copper average for the measured and indicated tonnes at Safari North.

At all three deposits, a primary copper-sulphide mineralization body is overlain by a blanket of copper carried in carbonates and oxides.

“Clearly there are a number of options: you can put the oxide through, you can stockpile the oxide and put the sulphide through, or you can do a combination of both,” McFadzean said. “One of the great advantages that we’re seeing with having three orebodies is that we have options. We’re working through those right now and we’ll take the most economic approach.”

Discussing the order in which to mine Kapulo’s deposits marks a big change for Mawson in a year. Signing the offtake and prepayment deal with Trafigura to fund the rest of the Kapulo build is the last step in Mawson’s mine-building, which saw the company take on a lot of debt to cover its capital needs and not turn a profit for several years.

In 2013 that changed: the company reduced its debt by almost US$28 million, leaving an outstanding US$7.5-million debt, and finished the year with US$48 million in the bank.

The company’s US$13.3-million net profit in 2013 helped. The company produced 20,948 tonnes copper and 1.94 million oz. silver, despite running out of open-pittable ore at Dikulushi in July and processing stockpiled material until underground operations got underway in November. It cost an average US69¢ to produce each pound of copper, net of silver credits.

With Dikulushi now an underground operation, costs have jumped. In 2014 Mawson expects to spend between US$2 and US$2.25 per lb. copper, or US$2.60 to US$2.85 per lb. excluding silver credits. The mine could produce 7,000 to 9,000 tonnes of copper in concentrate this year, based on current reserves lasting until the third quarter.

Dikulushi and Kapulo are 125 km apart. Both mines are on a 7,300 sq. km tenement in the DRC’s southeastern Katanga province. Mawson acquired the property in stages starting in 2006 and culminating in 2010, when it secured the 90% stake it holds today. Within a few months the company refurbished the Dikulushi processing plant and began treating the low-grade stockpile, which averaged 1.2% copper.

By mid-2011 Mawson had chewed through the stockpile and committed to establishing a new mine at Dikulushi, where reserves then stood at 539,000 tonnes grading 6.1% copper and 182 grams silver per tonne. In 18 months Mawson extracted 85% of those tonnes from an open pit.

The company went underground for the rest, and whatever new mineralization they could delineate. Underground drilling has been underway at the site since February, probing for more resources along the northeast-trending fault zone that hosts massive to semi-massive and fracture-disseminated copper sulphides.

On news of the Trafigura deal Mawson’s share price gained 10¢ in two days to close at 53¢. The company has a 52-week share price range of 34.5¢ to 73¢, and 171 million shares outstanding.

Be the first to comment on "Trafigura gives Mawson the money to build Kapulo copper mine in DRC"