Facing more restrictive foreign investment policies in developed markets, China is expected to continue building its influence over key minerals such as lithium and cobalt across the developing world, according to S&P Global.

In a recent report, the U.S. data analytics firm stated that “China’s reach is quietly growing behind minerals critical to a wide range of products that will shape the future,” with firms from upstream to downstream, from miners to battery makers to electric vehicle manufacturers, all jumping into this race.

“Whether related to top-line growth, cost control, supply security, or backward integration, their motivations are compelling and are likely to last beyond temporary dips in these minerals’ prices,” S&P stated.

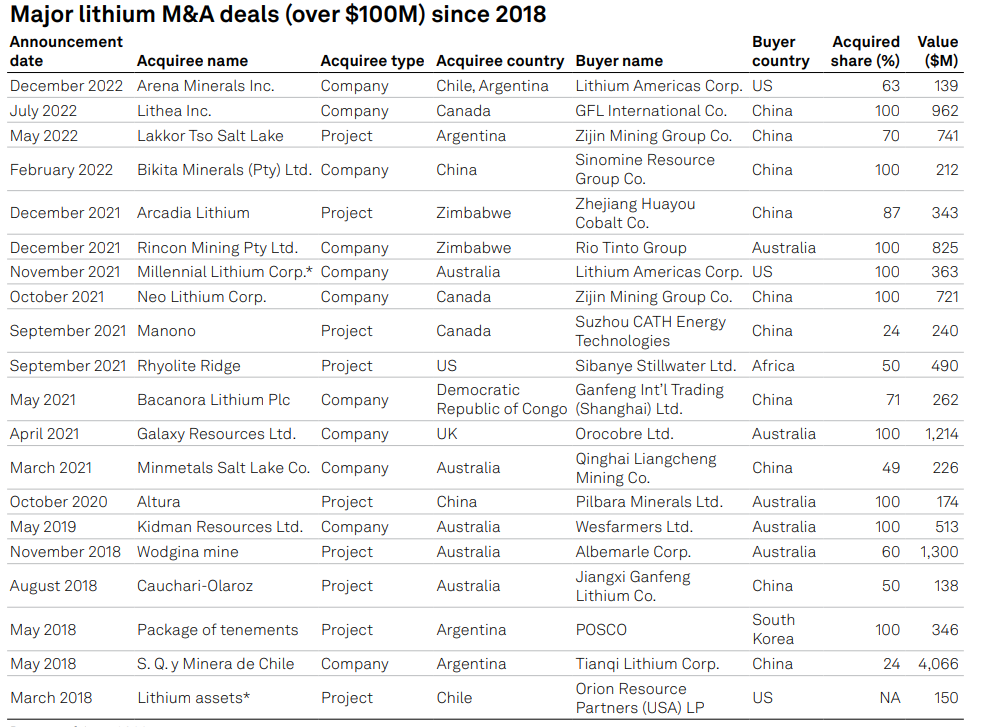

China leading lithium M&A

Although many countries — including the United States — are increasingly aware of these minerals’ importance, S&P analysts noted that it is China that has been the most active in these pursuits. This is evident in the number of mergers and acquisitions involving Chinese firms.

As shown in the table below, acquisitions of lithium assets by China’s mining majors and producers have accelerated since 2021, coinciding with the rise in lithium prices.

Credit: S&P Global

Lithium producers such as Ganfeng and Tianqi are trying to secure upstream raw materials for expanding production in their core business, while metal miners such as Zijin are just entering the lithium chase to diversify their exposure and to benefit from the mineral’s growth potential.

“Although demand from downstream EV markets has softened recently on slowing global growth, we expect interest in these minerals to persist and acquisitions to continue as firms across related industries grapple with supply security and cost volatility,” S&P said.

In addition to lithium, nickel and cobalt are also attracting investments from both Chinese upstream and midstream firms. However, these deals are smaller and are mostly in Indonesia and Australia.

Battery makers & OEMs

Also driving China’s investment push is the vertical integration of its battery makers into the upstream mining sector, the S&P report said.

Before 2021, when the EV penetration rate in China was still low at about 5%, the supply and demand for both battery and raw materials were largely balanced. Battery makers made small upstream investments by acquiring minority stakes in miners to strengthen their relationships and secure stable supply.

Since then, EV penetration rates in the country have exploded, rising to 15% in 2021 and 27% in 2022. However, the cost of lithium carbonate also escalated by at least tenfold during that period, S&P noted.

“In light of the significant supply shortages and surge in material costs in the last two years, more battery makers are trying to manage costs by establishing stronger ties with upstream players not just at home, but also abroad,” the report found.

In addition, Chinese auto OEMs are also venturing upstream as part of a backward integration push

that led them to develop in-house battery technologies. This trend is observable across some of the industry’s largest players including BYD, which have been acquiring minority stakes or setting up JVs with lithium miners and refiners.

Investment destinations

In terms of where Chinese firms tend to look for their critical minerals, Australia was initially the obvious destination, according to S&P. The country produced 363,309 metric tons of lithium carbonate equivalent (LCE) in 2022, accounting for 47% of global lithium raw material supplies.

However, challenges on the ground have increased due to more restrictive foreign investment policies. An example cited by S&P was Tianqi’s failed attempt to acquire the Australia-listed Essential Metals (ASX: ESS) earlier this year.

Chinese firms are facing similar challenges in Canada — not just for future projects, but also for existing investments — with the introduction of new rules last fall under the Investment Canada Act.

Instead, Chinese investors are now starting to shift towards emerging markets, in particular, Latin America and Africa, S&P said.

In 2022, Zijin bought controlling interests in two projects in China and completed the acquisition of Tres Quebradas in Argentina. Several others are now looking to follow suit.

Ganfeng is expanding its footprint in Argentina, China, Mali and Mexico. BYD is looking to invest in lithium projects in Chile, Argentina and Africa. CATL is leading a consortium to invest US$1.4 billion in Bolivia to build lithium extraction plants.

In Africa, “China has recently moved quickly to secure mining assets, often in conjunction with infrastructure development projects,” noted Len Kolff, interim CEO of Atlantic Lithium.

China’s outreach to deepen

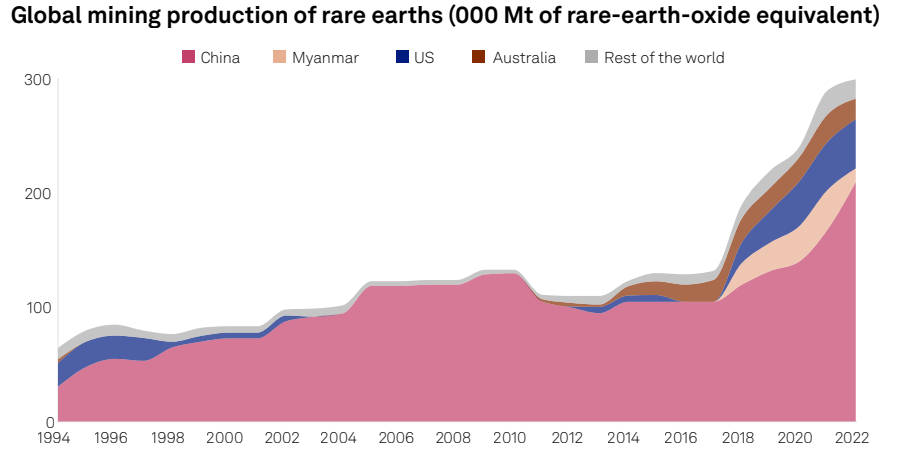

According to the S&P report, China’s control over critical minerals reach may deepen and broaden as it continues to build sizable market positions as owners, producers or offtakers. This not only applies to lithium, but other minerals as well.

This phenomenon is the most striking in rare earths, in which China now accounts for roughly 60% of the mining, 91% of refining and 94% of magnet production.

Another example is unfolding in the nickel market, where China’s “going out” strategy under the Belt and Road Initiative and Indonesia’s nickel ore export ban in 2020 have prompted firms to pour billions of dollars into Indonesia’s nickel supply chain in recent years, S&P wrote.

The findings in S&P’s report are in line with a study published by the Green Finance & Development Centre at Fudan University in Shanghai, which predicted that China’s overseas metals and mining investments this year could surpass the previous record of US$17 billion set in 2018.

Be the first to comment on "China zooms in on Latin America, Africa in critical minerals race, says report"