Talison Lithium (TLH-T, TLH-V) got a healthy boost from higher sales and production for the period ended Sept. 30. Its shares jumped 26.5% to $3.77 on the news.

For the period, classified as the first fiscal quarter of 2012, the miner sold 80,315 tonnes of lithium concentrate, or a 53% increase from the year-ago quarter.

It also ramped up its production of lithium concentrate from the year-earlier period by 12% to 90,708 tonnes.

Analyst Jonathan Lee of Byron Capital Markets tells The Northern Miner that preliminary sales and production numbers were in-line with his estimates, adding that the company is benefitting from operational tweaks.

“Talison is currently producing at capacity, and it continues to find small gains in production through operational efficiencies,” he writes in an email.

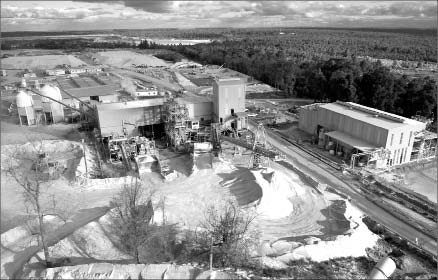

The company is expanding a processing plant at its Greenbushes Lithium Operation in Australia. The project has two plants, one for generating technical-grade lithium concentrates, and the other for chemical-grade lithium concentrates.

The latter plant is undergoing a stage-two expansion at a cost of $65 million to $70 million. Once completed, production capacity at Greenbushes is expected to double to 740,000 tonnes a year lithium concentrate, or 110,000 tonnes per year lithium carbonate equivalent.

“We believe that this will continue to show operational efficiencies with the modern plant and better efficiencies through scale,” Lee comments on the expansion. He reckons it will help Talison gain more market share and generate extra revenue while reducing its unit operating costs. As a result, margins will rise.

Based on a processing rate of 740,000 tonnes a year, the hard rock Greenbushes mine could produce for 22 years.

It hosts a reserve of 31.4 million tonnes grading 3.1% lithium oxide, with another 70.4 million tonnes at 2.6% lithium oxide in the measured and indicated resource categories

The chemical-grade plant, which should be running by the end of 2012, is garnering interest from new and existing customers.

“Talison continues to experience strong demand from customers across the world,” Peter Oliver, the company’s CEO, remarked in a press release. “This demand, together with a recent tightening in global lithium supply, is expected to enhance Talison’s pricing in the 2012 calendar year.”

In an Oct. 11 note, Lee mentioned that FMC (FMC-N) and Chemetall hiked up prices on their lithium products in July. He expects Talison to do the same, and notes that the producers saw more rains in South America, higher raw material costs and greater demand.

“Current market demand is rising as prices have increased over the last six months, and we believe that Talison will be able to fill the pent-up demand,” Lee elaborates in his email.

Responding to the global demand for lithium, which is driven by electric battery manufacturers, Talison is pushing to build a plant to convert lithium minerals into lithium carbonate. During the first stage, the plant could produce a maximum of 20,000 tonnes per year of lithium carbonate equivalent, before ramping up to 40,000 tonnes in the second stage.

While contemplating whether it should erect the conversion plant at Greenbushes or another location in Western Australia, Talison has retained an engineering consultant to estimate the plant’s start-up and operating costs. Those details should be

out by year-end.

At the Salares 7 project in Chile’s Region III, Talison plans to speed up its exploration program by injecting US$5 million in the second round of drilling. The program would include 5,000 metres, with an objective of outlining a resource estimate at Salar de la Isla.

To help develop its Chilean project, the company is setting up an office in Santiago.

By mid-November, the company will post its financial results for the quarter ended Sept. 30.

At presstime Talison shares traded at $3.55 within a 52-week range of $1.73-$7.80.

Byron Capital Markets has a “buy” rating on the stock and a target price of $6.55.

Be the first to comment on "A strong quarter for Talison"