Beaver Creek, Colo. – Gold’s fresh record above $3,660 per oz. flashed along with the $50-billion (C$69-billion) Anglo American (LSE: AAL)–Teck Resources (TSX: TECK.A TECK.B, NYSE: TECK) merger announcement Tuesday to turn the Precious Metals Summit into an investor pivot point towards physical assets.

Keynote speakers argued the yellow metal is moving from “portfolio insurance” to “performance engine” based on official-sector (central banks and sovereigns) buying. China’s demand and a bond-market bear also redraw the investing playbook.

“Good morning and happy new all-time high,” Ronald‑Peter Stöferle of Liechtenstein-based Incrementum AG, publisher of the In Gold We Trust report, said. “We are today’s contrarians. Welcome to the ‘Big Long’ now.”

Haven to horsepower

The classic 60/40 portfolio has broken down, Stöferle said. He proposed a new mainstream model with 45% equities, 15% bonds, 15% ‘safe‑haven gold,’ 10% ‘performance gold,’ 10% commodities and 5% Bitcoin.

Safe-haven gold is physical bullion stored in strong jurisdictions, a long-term insurance holding. Performance gold represents aggressive allocation – silver and gold/silver miner equities – managed actively.

“Safe‑haven gold carried us through pandemics, wars and deficits – now it’s time for performance gold to shine,” he said. The analyst said that the cycle has transitioned from contrarian accumulation to public participation, suggesting there is more room for the gold bull to run.

“The East is buying while the West is still asleep,” he noted, pointing to low allocations among Western institutions and renewed official‑sector demand.

Cash flows also typically migrate from majors to mid-tiers and, late in the cycle, to juniors, warning that mining equities are “not buy‑and‑hold – they must be timed,” Stöferle noted.

He explained that ‘performance gold’ entails investments in silver plus precious‑metal miners’ equities, used to amplify bullion’s uptrend. Investors historically rotate to miners and silver once the gold price clears resistance and mainstream investors join the trend.

Copper’s consolidation

The Anglo-Teck merger caused a stir of excitement on the conference floors. The deal is to create a top‑five copper producer with a primary London listing and headquarters in Vancouver.

If approved by regulators in Canada, the United States and China, the tie‑up would concentrate world‑class copper districts across Chile, Peru and Canada, and signals that scale and permitting scarcity are driving strategy. The move underlies the summit’s broader message that capital is voting for metals exposure, not just bullion.

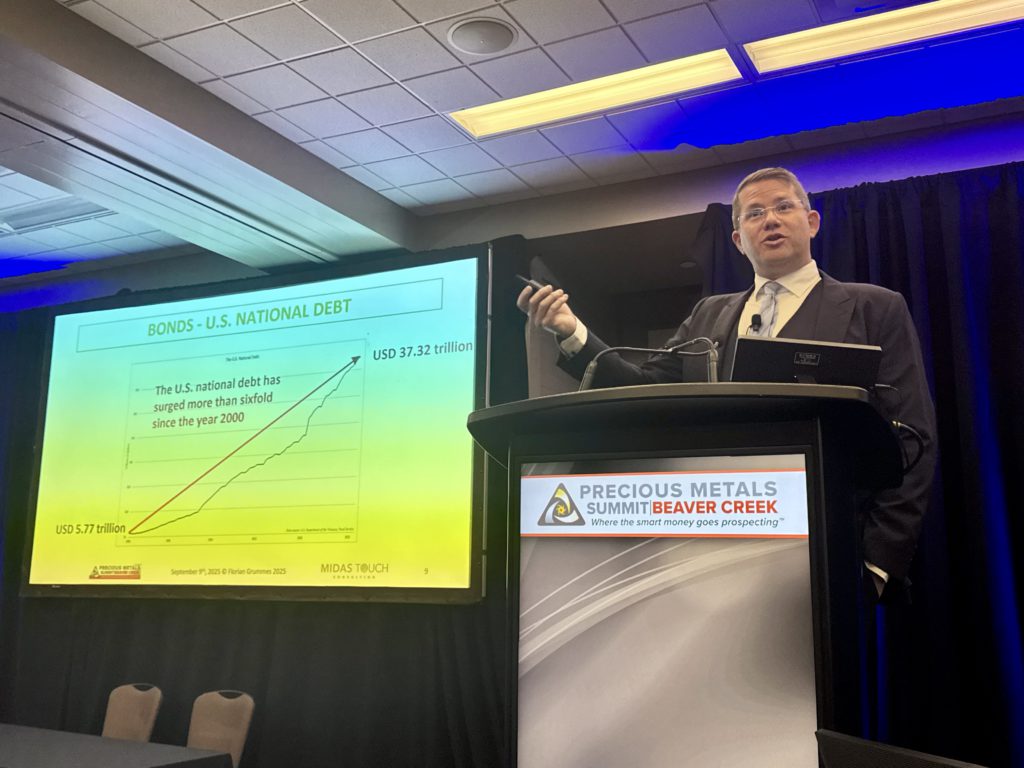

Independent analyst Florian Grummes of Munich-based Midas Touch Consulting framed the four drivers of the bull market. They are expanding liquidity across major economies; a bond‑market bear that is pushing allocators toward real assets; China’s bid, visible in strong physical demand; and persistent central‑bank purchases since 2022.

“Gold is being re‑monetized and this is not going to end anytime soon,” Grummes said.

He added a near‑term map for investors: momentum is “locked in” on daily charts, but the market is overbought, so relatively small pullbacks would be normal inside a trend, he cautioned.

Independent analyst Florian Grummes of Munich-based Midas Touch Consulting. Credit: Henry Lazenby

Silver’s shine

Silver has trailed the gold price higher to about $41.20 per oz. Tuesday in a series of bursts. Grummes cautioned against chasing vertical spikes but said a decisive break above $42.50 per oz. would be an “activation level,” potentially accelerating toward $50 “rather quickly.”

Stöferle’s macro lens was similar: silver is “cheap, tight and ‘performance gold’ ready to outperform,” with the gold–silver ratio at 88:1 (down from roughly 100:1 a few months ago) still above long‑run norms.

Mind the gaps

The speakers stressed discipline despite the euphoria.

China is due to shut for its so-called ‘Golden Week’ early next month and its big buyers of physical gold like jewellers, banks and retail investors will step away for a week. Trading in paper gold (futures and forwards in London and New York) thus has a bigger influence on price than usual, Grummes warned, so short bursts of selling can push quotes around more easily.

Once China reopens, the physical bid tends to reappear and can firm up the market again.

Grummes also flagged that miners are testing decade‑old resistance and sentiment is frothy. It’s not the time to chase even if there’s “no reason to short or do anything against this trend,” he said. “Don’t do this, please.”

The speakers noted that in broad risk‑off episodes, miners can be sold for liquidity even in a gold bull market.

Grummes further suggested investors scale out of some winners rather than exiting the sector.

“Pay yourself when the market makes money available,” he said, suggesting 10%–25% trims to fund dips, while Stöferle reiterated that timing tools matter for mining equities.

“Bull markets create wealth, timing preserves it,” he said.

Changing buyers

A common thread across the sessions in Colorado focused on who’s buying, and why. Central banks have posted three consecutive years of +1,000‑tonne net purchases, a trend reinforced by sanctions risk and reserve diversification.

China’s retail and exchange demand has become the marginal price setter, whereas Western family offices and pensions remain underweight. “At 2%, that’s not a hedge – it’s pocket change,” Stöferle said of typical investor allocations he sees.

What’s next

Near term, the speakers are watching how gold behaves around round numbers – $3,700 and $4,000 – whether sustained exchange-traded fund inflows finally reach the miners and juniors after years of outflows, and how the Anglo–Teck deal approvals – and any rival bids – telegraph how aggressively the industry is willing to pay for copper growth.

As Stöferle put it, the secular story is maturing, not peaking.

“The gold narrative is spreading, prices climb and consolidate, then climb again.” The caveat, from both speakers, is to embrace the trend without abandoning discipline.

Be the first to comment on "Beaver Creek: Gold, $50B copper deal bring reset"